Foreign Legal Consultant Hong Kong

"Lease financing is effectively a mainstream form of financing in the shipping space."

Prior to the advent of Chinese leasing, ship leasing was historically a financing structure in the alternative ship finance space. It was originally perceived as a relatively covenant free financing instrument which provided high financing leverage compared to what was provided at the time under traditional debt financing. It was frequently used as an off-balance sheet structure – something that changed with the introduction of IFRS 16 almost 10 years ago.

As Chinese leasing gained popularity, we saw the birth of various leasing houses around the globe. It is safe to say that nowadays lease financing is effectively a mainstream form of financing in the shipping space. It represents well more than a quarter of the total ship financing portfolio.

Unquestionably therefore, ship leasing is highly important to the industry. Shipowners nowadays around the globe order ships on the premise that these would be financed by way of a leasing structure (during and post construction). As leasing is not as heavily regulated compared to debt financing, lessors can offer both flexibility and very competitive terms. Leasing is also suitable in some cases for capital intensive projects, due to the abundance of available capital.

Evolution of leasing

The extensive adoption of ship leasing has led to a maturing of the product. There is a solid understanding of the intricacies of the various structures available in the market. However, clients’ needs continue to evolve.

Some shipowners, for various reasons, still grapple with the notion of relinquishing title to their assets in order to obtain financing. Lessors have also identified areas where leasing could have more robust enforcement of rights and areas where they wish to reduce operational risks of being “owners” of a vessel.

We have therefore been approached by various stakeholders in the industry to devise a solution whereby the title would remain with the lessee.

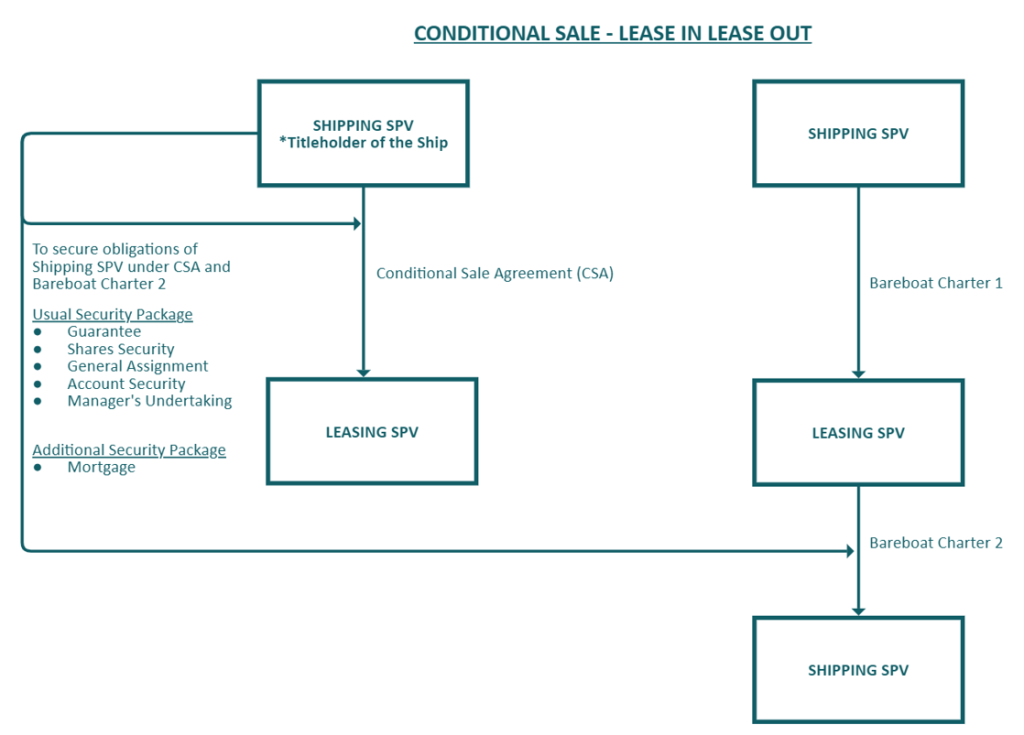

Conditional sale – Lease-in lease-out

Lease-in lease-out structures are not new in the market. We have seen them deployed in other asset classes, particularly in the aviation space, but also in shipping in the 80s/90s. The structure we have formed, shown in the diagram below, has developed from structures in the aviation space adapted to a shipping context:

Ownership – consideration

Key contacts

Partner Hong Kong

Foreign Legal Consultant Hong Kong

Partner London

Partner London

Partner New York

Partner New York

"The CSA provides a mechanism whereby such transfer of title shall be feasible at any time during the lease tenor if any such condition is met."

The financing amount is expressed as consideration for the acquisition of the Ship and will be paid under a Conditional Sale Agreement (CSA). The amount and manner in which such amount will be paid will of course depend on the nature of the financing. The title of the Ship shall remain with the Shipping SPV until certain conditions under the CSA are met (such as a termination event or event of default). The CSA provides a mechanism whereby such transfer of title shall be feasible at any time during the lease tenor if any such condition is met.

Leasing

Under Bareboat Charter 1 the Shipping SPV (as head lessor) bareboat charters the Ship to the Leasing SPV (as head lessee). Bareboat Charter 1 transfers the possessory rights of the Ship from Shipping SPV to Leasing SPV. At the same time the Leasing SPV will onward transfer such rights to the Shipping SPV under Bareboat Charter 2. Bareboat Charter 1 will be fully subordinated to Bareboat Charter 2. Bareboat Charter 1 will terminate automatically if title of the Ship is transferred to Leasing SPV.

Bareboat Charter 2 is similar to the charter utilised in the traditional sale and lease-back transaction. All ship and corporate-related covenants typically found in a finance lease are included in Bareboat Charter 2. The main differences between Bareboat Charter 2 and a standard finance lease are the CSA and the Mortgage in the security package.

Enforcement/Termination

Upon the occurrence of a termination event under Bareboat Charter 2, Leasing SPV shall be entitled to:

- exercise its rights under the CSA (i.e. register the title of the Ship in its own name);

- terminate Bareboat Charter 2; and

- repossess the Ship and, subject to the agreed termination mechanism set out in Bareboat Charter 2, sell the Ship or assume residual value; OR

- enforce its rights as mortgagee under the Mortgage and sell the Ship via judicial sale or by selling the Ship privately if permitted under the Mortgage and the relevant laws.

Pros and Cons

From a lessor’s perspective the main pros and cons of this structure are:

- PRO: the optionality provided in enforcement scenarios (namely, to obtain title under the CSA or enforce the mortgage which is not available in a typical sale and lease-back);

- PRO: enforcement of the Mortgage allows the Ship to be sold with clean title. Case law on mortgage arrest is extensive and robust. A mortgagee generally ranks ahead of all claims except for maritime liens (such as collision damage, salvage claims and crew’s wages) and the actual costs of the arrest (depending on the jurisdiction);

- PRO: the proposed structure mitigates certain risks the lessor would incur as shipowner in connection with the operation of the Vessel, including certain sanctions, EU ETS etc.; and

- CON: whereas in a traditional sale and leaseback the Leasing SPV is the owner and thus protected in the insolvency of Shipping SPV (except under the US Chapter 11 or similar) in a CSA+LILO the lessor is not the owner of the ship. However, the lessor/Leasing SPV is protected by the mortgage as a secured creditor.

From a Lessee’s point of view the position is relatively neutral from an enforcement point of view as the new structure does not seem to adversely affect its contractual rights/right at law when compared to the rights/position at law conferred under a traditional lease. On the contrary, as the lessee remains the registered owner for as long as it performs under Bareboat Charter 2, the operation of the Vessel becomes less cumbersome.

"Key stakeholders need to adapt quickly to meet new challenges and demands of both financial institutions and ship owners and operators."

Additional considerations

There are of course additional considerations which need to be taken into account, such as accounting, tax, beneficial ownership etc. Each case requires a bespoke analysis as to whether this is the most appropriate structure.

Conclusion

Ship financing and leasing never stops evolving. Key stakeholders need to adapt quickly to meet new challenges and demands of both financial institutions and ship owners and operators. We have had the privilege of assisting our clients in their journeys to achieve the best possible outcomes in terms of availability of finance and operational flexibility. We are therefore in a strong position to continue to develop new and robust models to meet clients’ needs.

Key contacts

Foreign Legal Consultant Hong Kong

Partner Hong Kong

Foreign Legal Consultant Hong Kong

Partner London

Partner London

Partner New York

Partner New York