Partner London

"In 2019 the Philippine government took a major step in the eventual rollout of OSW by awarding WESC for OSW projects."

This article aims to provide, at a high level, an analysis of the offshore wind market in the Philippines, both in terms of its potential development and its regulatory framework, to facilitate market participants considering entry into, or continued engagement with, that market. The contributors set out some key considerations and issues for such market participants to think about in connection with their investments in the Philippines offshore wind market.

Contributors

1. Philippine Government Targets

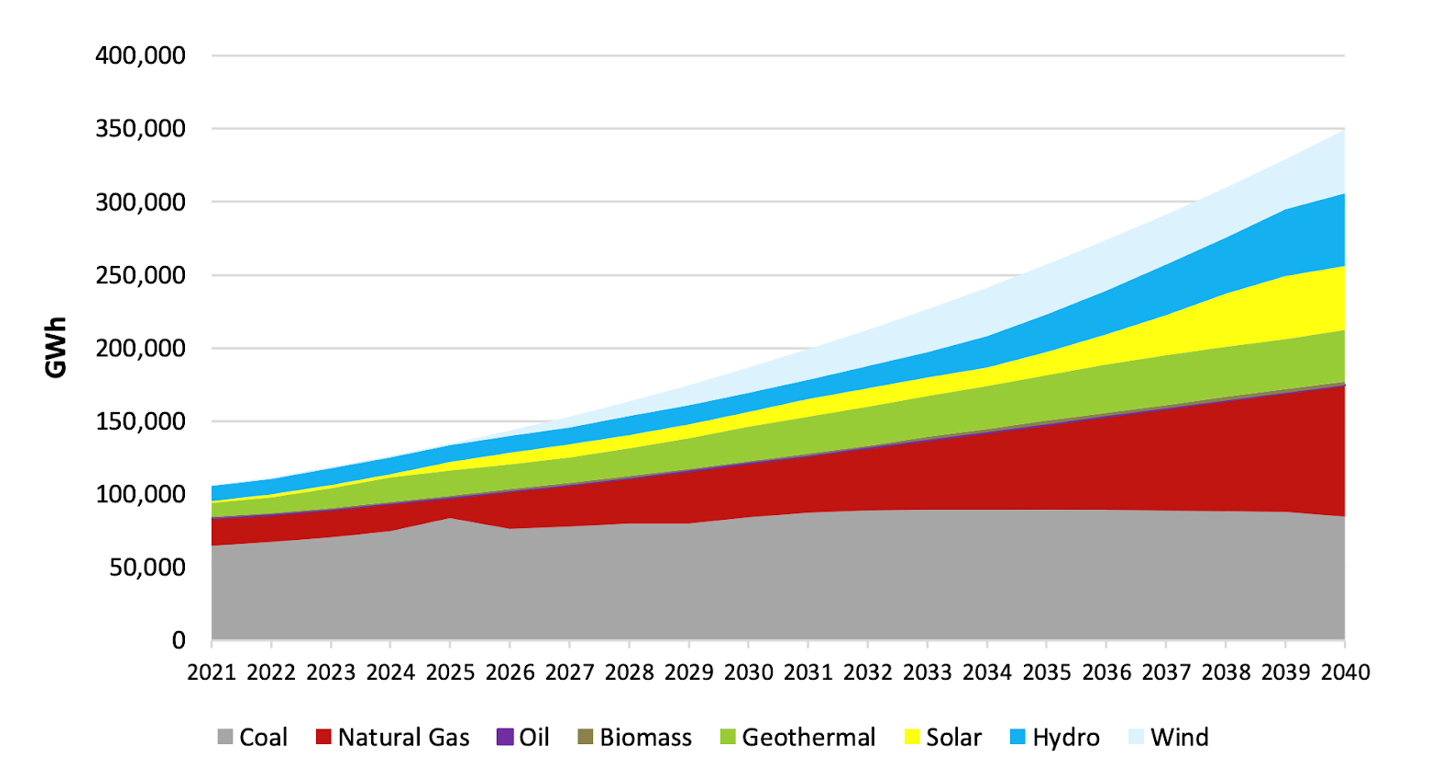

In 2019 the Philippine government took a major step in the eventual rollout of offshore wind (“OSW”) by awarding Wind Energy Service Contracts (“WESC”) for OSW projects. In the Philippine National Renewable Energy Program (“NREP”) 2020-2040, the government has pledged to achieve at least a 35% renewable energy share in the power generation mix by 2030 with aspirations to increase this to at least 50% by 2040 (Figure 1). This is consistent with the more ambitious ‘Clean Energy Scenario’ of the Philippine Energy Plan 2020-2040, contrasting with the alternative ‘Reference Scenario’ that sets a less ambitious target to achieve 35% renewable energy share in the power generation mix by 2040. OSW energy will play a significant role in achieving the clean energy scenarios set out in the NREP.

Figure 1: Philippines’ Power Generation Mix, 2021-2040, in GWh 35% by 2030 and 50% by 2040 (from NREP).

Achieving the NREP targets requires ramping up new-build capacities from renewables by 52.8 GW, including 16.7 GW from wind, 27.2 GW from solar, 6.2 GW from hydro, 2.5 GW from geothermal and 0.4 GW from biomass.¹

In 2022, the World Bank, in cooperation with the Philippine Department of Energy (“DOE”), published the ‘Offshore Wind Roadmap for the Philippines’,² providing strategic analysis of OSW development under hypothetical low- and high-growth scenarios. The low-growth scenario sees OSW accounting for 3.3% of the Philippines’ electricity supply by 2040; contrasted with 21% by 2040 in the high-growth scenario. The World Bank estimates a total of 178 GW wind energy potential within 200 km from the shoreline in the Philippines. Most of this potential (160 GW) is expected from floating wind turbine generators (“WTGs”) and the rest (18 GW) from fixed foundation WTGs.³

2. Philippine Offshore Wind Market

The OSW market in the Philippines is set for significant growth.⁴ Increasing interest in the Philippine OSW market is evidenced by several M&A deals, such as the acquisition by Ayala-backed ACEN Group of a 25% stake in CI GMF II Camarines Offshore Wind Energy Corporation. CI GMF II Camarines Offshore Wind is the holding company for CI NMF (PH) that will develop, construct, operate and maintain the Philippines’ first large-scale OSW farm. This transaction builds on ACEN’s earlier share purchase and loan agreement with Copenhagen Infrastructure Partners (“CIP”) that saw ACEN acquire a 25% stake in CIP’s proposed 1 GW Camarines Sur offshore wind project in the Philippines.

Key contacts

Partner Hanoi

Senior Associate London

Associate London

Partner Singapore

Partner Dubai

"The OSW market in the Philippines is set for significant growth."

Key factors driving this growth in the Philippine OSW market include:⁵

- technical potential: the World Bank estimate of a total of 178 GW wind energy potential within 200 km from shoreline in the Philippines means there is scope for development;

- government policies and targets: the DOE aims to achieve 2 GW OSW capacity between 2028 and 2030. Progressive policies, including the country’s first offshore wind auction (see GEA-5 below), increase investor confidence and the decision to lift restrictions on foreign ownership has driven a 20 GW surge in renewable energy projects.⁶ Notably, Green Lane certification introduced under Executive Order No. 18⁷ has also helped streamline permitting, enabling faster implementation of foreign direct investments; and

- awarded contracts: as of August 2024, there were 92 Offshore Wind Energy Service Contracts (“OWESCs”) awarded, representing 66 GW of capacity.

Current OSW Projects

Notable projects include:

- Northern Luzon (BuhaWind Energy Philippines): joint venture between PetroGreen Energy Corporation and Copenhagen Energy to develop a floating offshore wind farm offshore of Ilocos Norte that will produce 2 GW and is expected to be fully operational by 2030. BuhaWind Energy was awarded a pre-development environmental compliance certificate in June 2025 and secured grid connection approval in August 2025. This is one of three floating offshore wind farms being developed by BuhaWind in the Philippines. The other projects, Northern Mindoro and East Panay, are expected to be operational in 2031 and 2033 respectively;

- Central Luzon, South Luzon, Northern Luzon and Southern Mindoro (BlueFloat Energy): BlueFloat Energy, a Spain-based developer, secured four contracts for floating offshore wind project sites with a total capacity of 7.5 GW; and

- Guimaras Strait Wind Power Project (Triconti Southwind Corporation) and Guimaras Strait II Wind Power Project under (Jet Stream Windkraft Corporation): these projects were among the first awarded OWESCs by the DOE. The total target capacity of these projects is 1.2 GW and are expected to generate 3600 jobs.

In July 2025, the DOE announced that it would cancel the contracts of OSW developers that are delayed by more than three years due to developer default.⁸ This stricter approach indicates that the DOE will be demanding greater delivery discipline from OSW developers, which may become increasingly prevalent where OWESCs have been awarded without adequately considering project siting.

Competitive Renewable Energy Zones

Achieving high levels of wind integration requires co-ordinated planning of generation and transmission development. In 2020 the DOE launched its Competitive Renewable Energy Zones (“CREZ”) initiative.⁹ The purpose of this initiative is to identify the most economic renewable energy resource areas with high concentrations of cost-effective renewable energy and strong developer interest. Prioritising those areas helps overcome key barriers to development such as limited grid access, land use restrictions and regulatory hurdles, thereby reducing risk for private sector renewable energy investment. CREZ initially focussed on onshore wind and solar PV, supporting planning of transmission backbones and grid expansion in relation to those identified zones.

A 2025 study conducted by the US Department of Energy’s National Renewable Energy Laboratory in partnership with the DOE¹⁰ expanded the CREZ framework to incorporate offshore wind. This study recognised the need for integrated transmission planning to unlock these assets and provided three key insights:

- offshore wind has a more stable generation profile than onshore wind or solar PV, which is beneficial for grid operators and supports further grid integration;

- the offshore wind profile is geographically diverse and, of the offshore wind zones studied, most of the technical capacity consists of floating rather than fixed WTGs; and

- select onshore CREZs will be impacted by offshore wind, providing opportunities for strategic transmission investments in the Philippines.

Integrated planning will ensure that transmission capacity is available where generation potential is high and synchronised with the commissioning of OSW projects.

Transmission Development Plan

The latest National Grid Corporation of the Philippines’ Transmission Development Plan (“TDP”) is the TDP 2024-2050.¹¹ This identifies potential OSW development zones and includes plans to integrate OSW projects that are under development. Projects include: the PhP90.6bn 500 kV Batangas-Mindoro interconnection and backbone project to link Mindoro Island to the Luzon grid and support the integration of solar and onshore wind in CREZ; and OSW projects in the area between Mindoro and Panay islands. In southern Luzon, the 500 kV backbone will be extended to Tublijon, Sorsogon to accommodate onshore and offshore wind capacities.¹²

Port Infrastructure

One key enabler of OSW development that is often overlooked is port readiness. Unlocking the estimated 178 GW of technical offshore wind potential requires prioritising port infrastructure. The Philippine Ports Authority is set to repurpose three ports identified as critical to OSW development given their proximity to high-potential OWESCs. The Port of Currimao in Ilocos Norte, Port of Batangas in Sta. Clara, Batangas City, and Port of Jose Panganiban in Camarines Norte will be modernised to ensure they serve as logistical hubs for the installation, commissioning, and operation of OSW projects.

"On 19 April 2023, the President of the Philippines issued EO21 directing the DOE to establish the policy and administrative framework for OSW development."

3. Regulatory Framework

On 19 April 2023, the President of the Philippines issued Executive Order No. 21 (“EO21”) directing the DOE to establish the policy and administrative framework for OSW development.¹³ EO21 mandates a unified system for permitting in respect of OSW projects. Anchored upon EO21, in February 2025 the DOE (in collaboration with the Southeast Asia Energy Transition Partnership) published the ‘Compendium Guidebook to Permitting and Consenting for Offshore Wind Energy in the Philippines’.¹⁴ This provides a comprehensive overview of the permitting process for developing OSW in the Philippines. These identified permits will be integrated into the Energy Virtual One-Stop Shop (“EVOSS”) platform, promoting a transparent and streamlined service for energy related applications.

In relation to environmental permitting, the Department of Environment and Natural Resources (“DENR”) has issued dedicated rules (DENR Administrative Order 2024-02)¹⁵ for OSW developments. Applications for Environmental Compliance Certificates are handled by the DENR’s Environmental Management Bureau. The launch of the Fifth Green Energy Auction (“GEA-5”) also marks a significant milestone in Philippine OSW development by focussing exclusively on fixed-bottom offshore wind technology, setting a clear path for domestic and international developers in the industry. GEA-5 will offer an installation target of 3300 MW with a delivery commencement period from 2028 to 2030.

Foreign Investment

The Renewable Energy Act 2008 (Republic Act No. 9513) originally imposed Filipino ownership requirements on the exploration, development, and utilisation (“EDU”) of solar, wind, hydro and ocean or tidal energy resources. In 2022 the DOE issued Department Circular No. 2022-11-0034 which had the effect of amending the Implementing Rules and Regulations of the Renewable Energy Act 2008, enabling foreign investors to own up to 100% equity in Philippine entities engaged in the EDU of solar, wind, hydro and ocean or tidal energy sources. Furthermore, foreign investors can exercise full control over the operations and profits of these Philippine entities. The intention behind this amendment is to allow foreign investment in the renewables industry, accelerating progress to achieve 35% share in the renewable energy mix by 2030 and 50% by 2040.

Routes to Market

Routes to market for OSW generators include:

- Green Energy Auction Programme: this is the primary route to market for OSW projects in the Philippines. Under the current GEA-5, successful bidders will receive revenue certainty over a 20-year period from the Commercial Operation Date of their project under a Renewable Energy Payment Agreement (“REPA”);

- Bilateral Contracts: in the Philippines’ unbundled power market, power purchase agreements (“PPAs”) are typically made between developers and well-established retail distribution companies or government-backed entities;

- Wholesale Electricity Spot Market (“WESM”): WESM is the centralised electricity marketplace where OSW generators can sell excess energy not covered by a supply agreement or other bilateral contract. Electricity is offered in a ‘gross pool’ with prices governed by supply and demand that vary by location. OSW generators benefit from ‘must dispatch’ status, meaning their output is prioritised and automatically accepted onto the grid;

- Green Energy Option Program (“GEOP”): GEOP is a voluntary policy mechanism under the Renewable Energy Act 2008 that provides the option to qualifying end-users (generally with a monthly average peak demand of 100 KW and above for the past 12 months) to choose renewable energy as their source of energy. Renewable energy suppliers must: secure a Retail Electricity Supplier License from the Energy Regulatory Commission; secure Replacement Power Provision prior to applying Operating Permit to the DOE; and facilitate the registration and switching with the Central Registration Body; and

- Renewable Energy Market (“REM”): REM is a trading platform for Renewable Energy Certificates (“RECs”) which represent electricity generated from eligible renewable sources. Renewable energy generators earn RECs that are sold to suppliers to meet their Renewable Portfolio Standards.

It is expected that OSW projects will primarily utilise GEA-5 in the short-term. Longer-term options, such as PPAs, will require further cost reductions and derisking in the Philippine energy market.

4. Timeline

Development Process

"The development process for offshore wind projects in the Philippines begins by the developer obtaining a Certificate of Endorsement with the DOE."

The development process for offshore wind projects in the Philippines begins by the developer obtaining a Certificate of Endorsement with the DOE. This is accompanied by other registrations and approvals, such as business registration with the Securities and Exchange Commission and tax registration with the Bureau of Internal Revenue. The developer is also required to post a performance bond, being 2% (or 1% if not using a port administered by the Philippine Ports Authority) of the project cost per MW, multiplied by the offered capacity in MW according to the GEA-5 Terms of Reference.¹⁶

The next stage of the development process is pre-development. The developer must obtain an OWESC from the DOE as well as endorsements or permits from other agencies (including the DENR and National Commission on Indigenous Peoples) to ensure the project is environmentally sound, socially accepted, and technically feasible. Upon receipt of a Certificate of Confirmation of Commerciality from the DOE, the project commences its construction and commissioning phase. At this point, the Wind Energy Operating Contract (“WEOC”) is issued granting legal authority to generate and sell electricity.

The project must receive a further Certificate of Endorsement from the DOE and may enter several other agreements. For example, a Connection Agreement with the National Grid Corporation of the Philippines is required to connect to the grid. The project may also register with WESM via the Philippine Electricity Market Corporation, obtain a Certificate of Compliance and Feed-in Tariff eligibility from the Energy Regulatory Commission (“ERC”), and enter a REPA with the payment agent National Transmission Corporation (“TransCo”) if supplying under a Green Energy Auction Program.

GEA-5 Auction

On 11 June 2025, the DOE officially launched GEA-5 focussed exclusively on fixed-bottom OSW technology with an installation target of 3300MW between 2028-2030.¹⁷ Prior Green Energy Auction rounds did not include OSW, so this marks a major shift signalling the country’s intent to tap into its vast OSW potential. Fixed-bottom offshore wind was chosen due to its established global track record, cost-effectiveness and scalability.

Whilst the DOE acknowledges the future potential of floating offshore wind, the decision to prioritise fixed-bottom technology reflects a strategic effort to build early momentum. Current technical capabilities, regulatory frameworks, and infrastructure readiness make it the most viable pathway for successful deployment at this stage. If successful, GEA-5 is expected to attract significant foreign investment and position the Philippines as a regional leader in OSW.

The allocation framework methodology for GEA-5 incorporates price and non-price criteria, including price competitiveness, project readiness and capacity.¹⁸ In terms of the auction timeline, the DOE is yet to publish the Notice of Auction and the green energy auction reserve price is pending finalisation, so further delays are expected.

Figure 2: Prescribed timeline for GEA-5 (D = Day).¹⁹

| Activity | Tentative Timeline |

|---|---|

| DOE Issuance/Posting of List of Winning Bidders/Notice of Award | D99 + 1 working day |

| Auction Proper | D68 + 1 working day |

| Pre-Bid Conference | D49 + 2 working days |

| Notification to Qualified Bidders on successful registration and to Qualified Suppliers who failed the evaluation | D38 + 1 working day |

| Last day of Registration | D32 + 3 working days |

| Start of Registration of Qualified Suppliers | D31 + 1 working day |

| Publication of Notice of Auction and Terms of Reference | D1 |

5. Key Issues and Considerations

"Government policies and targets aimed at promoting the OSW industry in the Philippines is a key factor driving growth in the market."

We set out below certain key issues for investors to consider in entering the offshore wind market in the Philippines:

- government support: government policies and targets aimed at promoting the OSW industry in the Philippines is a key factor driving growth in the market. OSW will play an important role in achieving the broader government target of 35% renewable energy share in the power generation mix by 2030. Equally, the DOE aims to achieve 2GW OSW capacity between 2028 and 2030. Progressive targets backed by policies, such as GEA-5, will promote investor confidence. The country is positioning itself to become a regional leader in the offshore wind market;

- infrastructure and technological readiness: the CREZ initiative has laid the groundwork for co-ordinated grid planning to assist the identification of the most economic renewable energy resource areas with high concentrations of cost-effective renewable energy and strong developer interest. However, port readiness remains a central challenge to the OSW market. Good port infrastructure could host local manufacturing and offer supply chain capability relevant to some areas of OSW. Another challenge concerns the suitability of the Philippines for floating rather than fixed-bottom WTGs. Although GEA-5 focuses on fixed-bottom technology, most of the country’s OSW technical potential is expected from floating WTGs and many OSW zones are better suited to floating WTGs. Globally, floating WTGs remain in the early stages of development;

- financing and bankability: long development timelines and the capital-intensive nature of OSW projects pose financial risks and challenges. Whilst the REPA under GEA-5 offers revenue certainty, investors should evaluate the bankability of these agreements. TransCo is the designated administrator of the GEA-All Fund. In March 2025 the ERC introduced a standardised REPA and released formal guidelines for the collection and disbursement of the GEA-All Fund to ensure timely and transparent payments to investors. The intended effect is to create a more predictable and reliable financing structure for developers to encourage investment;

- permitting and compliance: permitting remains complex meaning investors should engage early with government bodies to avoid delays. For example, developing OSW projects in or near marine protected or historical and cultural areas will have implications on permitting and clearance requirements. In this regard, marine spatial planning (“MSP”) can be used to mitigate conflicts with other marine uses. To support this, UK PACT is funding a project to technically validate and peer review the offshore wind MSP tool in the Philippines with the aim of enhancing industry confidence.²⁰ The Compendium Guidebook to Permitting and Consenting for Offshore Wind Energy in the Philippines represents a step towards detangling the permitting process. Integration of identified permits into the EVOSS platform will also promote a transparent and streamlined service for energy related applications; and

- geographic and climate risk: Tthe Philippines is prone to extreme weather such as typhoons and high seismic activity which poses operational risks to OSW infrastructure. It is likely that typhoon-class WTGs will be needed in many locations and certain locations will be particularly high-risk to extreme weather events that will be exacerbated by future climate change.

WFW London Trainee Kate McMahon also contributed to this article. Additional contributors were provided by Ivan Savitsky, Oliver Patrick and Kalyani Basu from The Carbon Trust and Kiril Caral from Gorriceta Africa Cauton & Saavedra.

[1] NREP p19.

[2] https://legacy.doe.gov.ph/sites/default/files/pdf/announcements/Philippine-Offshore-Wind-Roadmap.pdf

[3] https://documents1.worldbank.org/curated/en/716891572457609829/pdf/Going-Global-Expanding-Offshore-Wind-To-Emerging-Markets.pdf

[4] https://ctprodstorageaccountp.blob.core.windows.net/prod-drupal-files/2025-03/PHORA%20State%20of%20the%20OSW%20Market_March25%20approved%20version.pdf

[5] https://ctprodstorageaccountp.blob.core.windows.net/prod-drupal-files/2025-03/PHORA%20State%20of%20the%20OSW%20Market_March25%20approved%20version.pdf

[6] https://powerphilippines.com/doe-reports-20-gw-surge-in-renewable-projects-after-lifting-foreign-ownership-limits/

[7] https://boi.gov.ph/executive-order-no-18/

[8] https://business.inquirer.net/533614/doe-vows-to-cancel-offshore-wind-projects-delayed-by-3-years

[9] https://legacy.doe.gov.ph/renewable-energy/ready-renewables-grid-planning-and-competitive-renewable-energy-zones-crez

[10] https://www.osti.gov/biblio/2522773

[11] https://www.ngcp.ph/Attachment-Uploads/TDP%202024-2050%20FINAL%20REPORT-2025-03-11-10-41-01.pdf

[12] https://reglobal.org/philippines-grid-expansion-ngcp-focuses-on-renewables-integration/

[13] https://legacy.doe.gov.ph/sites/default/files/pdf/issuances/20240419-EO-21-FRM.pdf

[14] https://legacy.doe.gov.ph/sites/default/files/pdf/announcements/OSW%20Guidebook.pdf

[15] https://eia.emb.gov.ph/wp-content/uploads/2024/02/DAO-2024-02-OSW-Guidelines.pdf

[16] https://prod-cms.doe.gov.ph/documents/d/guest/annex-b-bonds_gea-5-_22082025-pdf

[17] https://legacy.doe.gov.ph/press-releases/doe-kicks-green-energy-auction-fixed-bottom-offshore-wind

[18] https://prod-cms.doe.gov.ph/documents/d/guest/annex-i-price-and-non-price-criteria-2025-08-19-pdf

[19] https://prod-cms.doe.gov.ph/documents/d/guest/3-draft-gea-5-noa-22082025

[20] https://www.ukpact.co.uk/country-fund/philippines

Key contacts

Partner London

Partner Hanoi

Senior Associate London

Associate London

Partner Singapore

Partner Dubai