WHERE ARE WE NOW?

Nearly a year on from the publication of the UK’s Hydrogen Strategy in August 2021 (see our analysis here), what progress have we seen? With commitments through to 2030, we focus here on the promises that the Hydrogen Strategy made for 2021/2022. These should, of course, be considered in light of the increasingly ambitious targets set out in the British Energy Security Strategy published in April 2022 (see our analysis here); it doubled the capacity ambition set out in the Hydrogen Strategy, with the goal now increased to 10 GW of low carbon hydrogen production capacity by 2030, with at least half of this coming from electrolytic hydrogen.

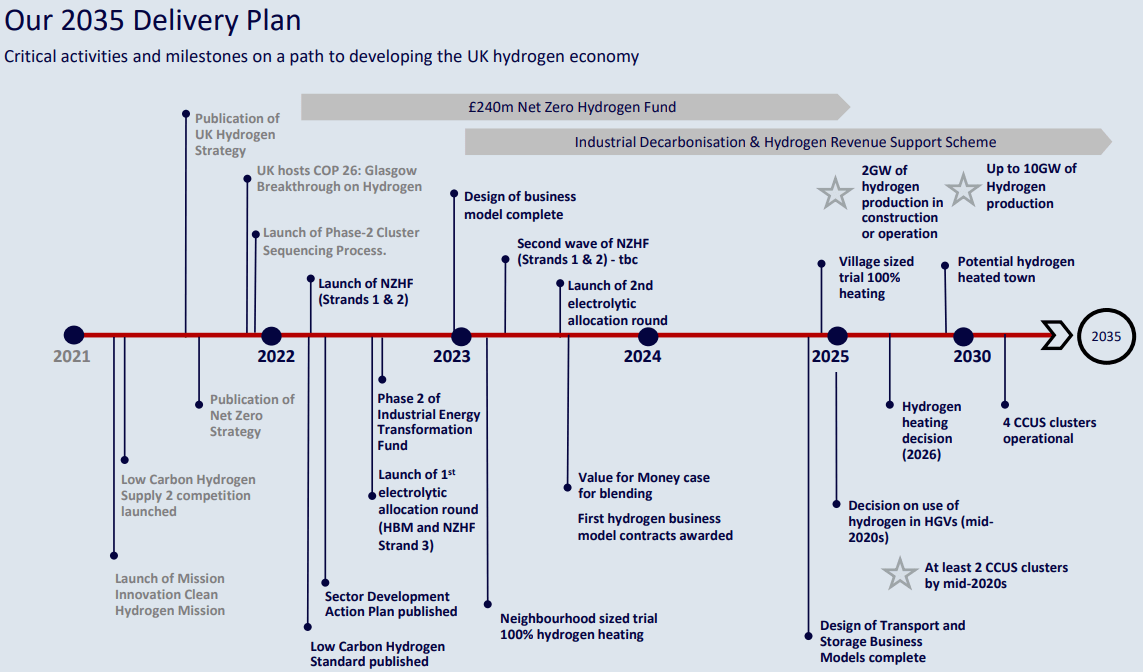

In a separate publication on 8 April 2022, the Hydrogen Investor Roadmap, the UK Government (the “government”) summarised the policies “designed to support the development of a thriving UK low-carbon hydrogen economy”. Stakeholders may find this a useful tool for tracking progress. It includes (on page 5) a delivery plan that may be useful to refer to alongside our analysis that follows:

By the “end of 2021”, the Hydrogen Strategy committed the UK government (the “government”) to the following measures.

| Commitment | WFW Comment |

|---|---|

| Launch a call for evidence on ‘hydrogen-ready’ industrial equipment. | A call for evidence that was more limited in scope (boilers only) launched 20 December 2021 and closed on 14 March 2022. Halfway through 2022, responses were still being analysed by government. |

| Launch a £55m Industrial Fuel Switching competition in 2021. | Done in August 2021, on the date the strategy was published. |

| Aim to consult in 2021 on ‘hydrogen-ready’ boilers by 2026. | The only consultation was for industrial hydrogen-ready boilers, rather than domestic ones. As set out above, this consultation closed on 14 March 2022, and a response has not yet been published. |

| Launch a call for evidence on the future of the gas system in 2021. | No update as of publication of this article. |

| Set out further detail on the revenue mechanism which will provide funding for the Low Carbon Hydrogen Business Model in 2021. | The proposed pricing mechanism was set out in the Government response to the consultation on a Low Carbon Hydrogen Business Model, published in April 2022. Indicative Heads of Terms for the business model contract were published alongside the response. |

| Establish a Hydrogen Regulators Forum in 2021. | According to parliamentary questions, this met for the first time in January 2022, though it does not yet have a separate internet presence. |

Policy and regulatory direction regarding the future of the gas systems in the UK will be a key step toward providing clarity and certainty for investors and stakeholders. It will also be important for the government to allow stakeholders to air their views and concerns, and to take steps to address these. Given the government’s reliance on the market and industry participants to meet its decarbonisation targets, it will have to ensure that industry voices are heard and that barriers and challenges are addressed to enable stakeholders and investors to overcome them and deliver. Halfway through 2022, we have not yet seen the promised Call for Evidence referred to in the table above, which is no doubt eagerly awaited.

The government response to the consultation on a Hydrogen Business Model (the “Business Model Response”) also referred to in the above table confirms the intention to proceed with a contractual, producer-focussed business model, which will apply to a range of hydrogen production pathways (though it is not intended to support existing producers seeking to retrofit using carbon capture, usage and storage technology, nor the production of by-product hydrogen).