Partner London

"In this article, our aviation and energy specialists explore how the different SAF regulations impact different flight plans into and out of the EU and the UK."

In our first article of this series, we compared the Renewable Transport Fuel Obligations (Sustainable Aviation Fuel) Order 2024 (“UK SAF Mandate”) and the ReFuelEU Aviation Regulation (“ReFuelEU”) (together, the “SAF Mandates”) and its application to different stakeholders in their respective jurisdictions.

In this article, our aviation and energy specialists explore how the different sustainable aviation fuel (“SAF”) regulations impact different flight plans into and out of the EU and the UK.

We also explain how the SAF Mandates interact with the key mechanisms for regulating greenhouse gas emissions, notably (i) the Carbon Offsetting and Reduction Scheme for International Aviation (“CORSIA”); (ii) the UK Emissions Trading Scheme (“UK ETS”); and (iii) the EU Emissions Trading Scheme (“EU ETS”).

SAF in context: How do the SAF Mandates interact with the key mechanisms for regulating greenhouse gas emissions?

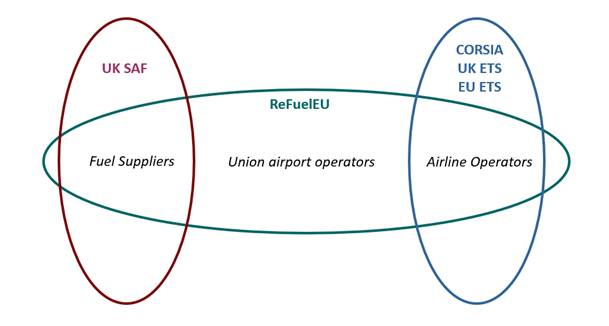

It is worth clarifying how the SAF Mandates fit into the broader greenhouse gas emissions regulatory landscape. The UK ETS and EU ETS are frameworks designed to reduce greenhouse gas emissions generally, across a breadth of sectors, and thereby impose obligations on a broad range of stakeholders. CORSIA and the SAF Mandates specifically target the aviation sector; CORSIA sets greenhouse gas emission reduction targets for airline operators on a global scale; the UK SAF Mandate imposes obligations on fuel suppliers in the UK supplying relevant aviation fuel, and ReFuelEU imposes obligations on fuel suppliers, airline operators and union airport operators in the EU.

In the aviation sector, CORSIA, UK ETS, and EU ETS impose obligations on airline operators, not fuel suppliers. As a result, stakeholders subject to the UK SAF Mandate (suppliers) do not face overlapping obligations under CORSIA and UK ETS. By comparison, airline operators subject to ReFuelEU are also subject to overlapping obligations under CORSIA and EU ETS.

The EU has designed a separate emissions trading system – ETS2 – to regulate the carbon content of fuels used in buildings, road transport and small industry by placing compliance obligations upstream on fuel suppliers. It is scheduled to start in 2027, with a possible delay to 2028 if energy prices remain unusually high. However, for the avoidance of doubt, whilst ETS2 covers fuels such as petrol, diesel, natural gas, heating oil, etc. it does not include jet fuel for aviation and does not therefore apply to SAF (or other jet fuel) suppliers.

High level overview of the five regulations

(a) International SAF/carbon emission regulations affecting the aviation sector

CORSIA is the International Civil Aviation Organization’s (“ICAO”) global market-based scheme designed to reduce carbon emissions in the aviation sector. It is the first global market-based scheme to apply to one . Like ReFuelEU, EU ETS and UK ETS, it applies to airline operators, but only in relation to international flights between ICAO member states (with the exception of humanitarian, medical and firefighting flights, all international civilian operations of aeroplanes are covered). Like EU ETS and UK ETS, it does not directly impose specific SAF obligations; its goal is to reduce greenhouse gas emissions.

However, the regulations clearly work together to ultimately achieve the same end-goal. SAF can reduce carbon dioxide emissions across its lifecycle by 80% in comparison to traditional jet fuels. Thereby, compliance with the SAF regulations improves a stakeholder’s ability to meet its objectives under CORSIA (and the ETS Regulations).

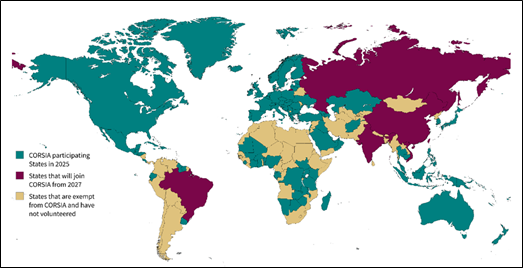

The first phase (2024 to 2026) is not mandatory; 129 ICAO member states, including the UK and the EU member states are currently participating in it (as shown below). The second phase, which is set to come into effect from 1 January 2027, is mandatory (with limited exceptions) for all 193 ICAO member states.

Airline operators who have opted-into the first phase and have annual emissions greater than 10,000 tonnes of carbon dioxide, must measure and report their carbon dioxide emissions from international flights and buy carbon credits from approved projects to offset the amount of carbon dioxide they emit in a given year to the extent that these amounts exceed 85% of the amount that they emitted in 2019.

Although airline operators subject to CORSIA are not directly subject to the UK SAF Mandate, it is in their interest to order increasing proportions of SAF from their suppliers so long as the higher cost of SAF does not outweigh the costs savings from not having to buy carbon credits to comply with CORSIA.

CORSIA Participating States

(b) ReFuel EU and carbon emission reduction regulations affecting the aviation sector in the EU

ReFuel EU emanates from ‘Fit for 55’ framework and sets mandatory targets for the aviation sector to reduce its carbon emissions. You can find a detailed overview of these in our first article.

The first comprehensive policy framework to apply a price to carbon from aviation emissions, and thereby even the playing field between the cost of fossil-based jet engine fuel and SAF, was the EU ETS. Under this regulation, airline operators must surrender allowances for each tonne of carbon emitted. It provides for a cap-and-trade system that allows airline operators to trade emission credits between them to meet their respective climate targets.

The EU’s Carbon Border Adjustment Mechanism (“EU CBAM”) is the EU’s scheme to place a price on carbon emitted during the production of carbon-intensive goods (including aluminium, steel, electricity and hydrogen) entering the EU and is being gradually introduced in line with the phase out of allowances under EU ETS. As modern aircraft are made primarily from aluminium and steel alloys, they will be directly impacted by EU CBAM. It is expected that EU CBAM will include petroleum products by 2030.

"To demonstrate compliance with the obligations, relevant suppliers must either apply for SAF Certificates or pay the buy-out price."

(c) UK SAF and carbon emission regulations affecting the aviation sector in the UK

Similar to ReFuelEU, the UK SAF Mandate imposes mandatory SAF blending obligations on qualifying fuel suppliers. To demonstrate compliance with the obligations, relevant suppliers must either apply for SAF Certificates or pay the buy-out price. To obtain the former, fuel suppliers must show that their fuel is both eligible and sustainable.

The UK ETS also operates a cap-and-trade scheme wherein a limit is set on the total greenhouse gas emissions from sectors covered by the scheme, including the aviation industry. It came into force on 1 January 2021, following the UK’s withdrawal from the EU, and supersedes the EU ETS for UK flight plans, although it preserves many of the features from EU ETS. Importantly, eligible SAF is ‘zero-rated’ fuel under both the UK ETS and the EU ETS, which means aircraft operators may be exempt from surrendering emissions allowances in relation to their use of qualifying SAF.

The UK Carbon Border Adjustment Mechanism (“UK CBAM”) is similar to EU CBAM, in that it covers emission intensive goods imported into the UK, including aluminium, steel and hydrogen from 1 January 2027. The introduction of other emission intensive goods is under review.

*

Both EU ETS and UK ETS place a cap on total emissions, whilst ReFuelEU and UK SAF impose an obligation to meet a minimum SAF threshold, but all four regulations allow for a level of flexibility that enable the relevant stakeholders to meet their obligations by trading certificates between them. Those airline operators who go above and beyond their obligations can make a profit, whilst those who fall short are able to pay a fee to attribute other airline operators’ compliance to themselves, thereby also meeting their own obligations.

On 19 May 2025, the UK and EU announced plans to link and to align the UK ETS and EU ETS regimes and on 16 December 2024, the UK government issued a consultation on the incorporation of CORSIA into UK law, with the aim of maximising compliance with CORSIA in a form consistent with UK ETS.

How different flight paths are affected under the different SAF/carbon reduction regimes in the aviation sector?

The map below¹ is designed to show how the regulations apply depending on the flight path taken by the aircraft with which the relevant stakeholders are involved.

Image Credit: European Union

Flight plans into and out of the EU

- Flight Plan A: aircraft flying from the EU to outside the EU/EEA: CORSIA applies to the relevant airline operator (where the destination is an ICAO member state) and ReFuelEU applies to (i) the fuel supplier fuelling the flight; and (ii) the departure union airport;

- Flight Plan B: aircraft flying from outside the EU/EEA into the EU/EEA: CORSIA applies to the airline operator (where it originates from an ICAO member state);

- Flight Plan C: flights within EU/EEA countries: Both EU ETS and ReFuelEU apply to the airline operators, and ReFuelEU also applies to (i) the departure union airport; and (ii) the qualifying fuel suppliers;

- Flight Plan D: aircraft flying from the UK into the EEA: UK ETS applies to the relevant airline operators and the UK SAF Mandate applies to the relevant fuel suppliers;

- Flight Plan E: aircraft flying within the UK: UK ETS applies to the relevant airline operators and the UK SAF Mandate applies to the relevant fuel suppliers;

- Flight Plan F: aircraft flying from the UK to outside EEA – CORSIA and UK ETS apply to the relevant airline operators (where destination an ICAO member state, in the case of CORSIA) and UK SAF applies to fuel suppliers in relation to the fuel supplied in the UK; and

- Flight Plan G: aircraft flying from outside the EEA into the UK – CORSIA applies to airline operators (where these originate from an ICAO member state) and UK SAF applies to fuel suppliers but only to the fuel supplied in the UK (in this context, for refuelling at UK airports, for example).

Example

To provide a more comprehensive example, imagine an aircraft that first flies (Flight 1) from New York to London, then (Flight 2) from London to Edinburgh, then (Flight 3) from Edinburgh to Paris, then (Flight 4) from Paris to Frankfurt, and finally (Flight 5) from Frankfurt to New York.

Flight 1: CORSIA would apply to the airline operator.

Flight 2: UK ETS applies to the relevant airline operators and the UK SAF Mandate applies to the relevant fuel suppliers if fuel was being provided in the UK in preparation for Flight 2 (if the airline has enough fuel to proceed onto Edinburgh without refuelling at this stage, UK SAF Mandate does not bite).

Flight 3: UK ETS applies to the relevant airline operators and the UK SAF Mandate applies to the relevant fuel suppliers if fuel was being provided in the UK in preparation for Flight 3 (if the airline has enough fuel to proceed onto Paris without refuelling at this stage, UK SAF Mandate does not bite).

Flight 4: Both EU ETS and ReFuelEU apply to the airline operators, and ReFuelEU also applies to (i) the departure union airport; and (ii) the qualifying fuel suppliers.

Flight 5: CORSIA applies to the relevant airline operator (since the USA is an ICAO member state) and ReFuelEU applies to (i) the fuel supplier fuelling the flight; and (ii) the departure union airport in Frankfurt (Frankfurt Main or Frankfurt Hahn).

Navigating the different environmental regulations applicable to the aviation sector is complex, as the regulations listed above – whilst being complementary – were not designed in a unified way.

The relevant industry stakeholders need to continuously monitor their compliance with the regulations, as and when they may apply depending on the flight plan the aircraft takes. Given that each regulation imposes its own eligibility requirements, sustainability and monitoring, verification and reporting requirements and compliance rules, this is no straightforward feat.

Below we highlight a few of the key differences in terms of eligibility criteria for sustainable aviation fuels (“SAF”) and whether carbon offsets or ETS allowance trading is permissible under each of CORSIA, UK ETS, EU ETS, and the SAF Mandates.

SAF Eligibility Criteria

| Regime | What is covered | Eligible Fuels | Carbon emission reduction requirement | Carbon Credit offsets / ETS allowances trading |

|---|---|---|---|---|

| CORSIA (International) | Global scheme for aviation emissions under ICAO. Applies to international flights. | SAF or lower carbon aviation fuel. SAF production accepts a wider range of feedstocks (including certain crop-based materials) than the other schemes listed below. The feedstocks must not come from land or water systems with high carbon stock. Additional sustainability criteria apply, for example, water, soil, air, conservation, human rights and food security. | At least 10% reduction compared to fossil jet fuel. | Carbon credits can be used via Eligible Emissions Units (“EEUs”) approved by CORSIA. |

| UK ETS | UK Emissions Trading Scheme for aviation emissions from applicable flights. | Addresses aviation emissions from applicable flights rather than fuel type. SAF has a zero-emission factor under UK ETS. | SAF must achieve ≥40% GHG reduction vs fossil fuel. | ETS allowances may be traded SAF certificates cannot offset ETS targets. |

| EU ETS | EU Emissions Trading Scheme for aviation emissions from applicable flights. | Same as UK ETS – addresses emissions from flights, not fuels. SAF has a zero-emission factor under EU ETS. | No specific % stated (zero-emission factor applies). When an airline uses SAF, the associated CO₂ emissions are considered zero, so they don’t need to surrender ETS allowances for those emissions. Airlines get the full emissions benefit from SAF use - every litre counts without needing to meet a minimum reduction threshold. This creates a strong financial incentive to use SAF, as it reduces compliance costs under ETS. | ETS allowances may be traded. SAF certificates cannot offset ETS targets. |

| UK SAF Mandate | UK mandate requiring a minimum share of SAF in aviation fuel supply. | SAF from biomass, waste, residues; power-to-liquid fuels (renewable or nuclear-derived); recycled carbon fuels; low-carbon hydrogen. Crop-based biofuels not eligible. HEFA-based fuel is capped at specific percentages of the total SAF obligation (100% in 2026, gradually decreasing to 71% by 2023). The intention is to encourage suppliers to use newer SAF technology - like power-to-liquid or fuels from municipal waste -which tend to have higher greenhouse gas savings (often achieving 60-70% reduction compared with 40% for HEFA) Fuels must meet defined environmental and social standards to qualify under government incentives. These are typically verified through a sustainability certification or life-cycle assessment (LCA) process. | ≥40% GHG reduction vs fossil fuel (baseline: 89 gCO₂e/MJ). | SAF certificates transferable only for compliance with SAF mandate. |

| EU SAF Mandate (ReFuelEU) | EU mandate requiring SAF blending in aviation fuel. | SAF from waste/residues, recycled carbon fuels, synthetic fuels (renewable hydrogen + captured carbon). Crop-based biofuels not eligible. Sustainability criteria apply. | ≥70% reduction for synthetic fuels; ≥65% for biofuels (baseline: 94 gCO₂e/MJ). | SAF certificates transferable only for compliance with SAF mandate. |

Importantly, the table above shows that there are variances as regards fuel eligibility criteria, sustainability criteria and carbon emission reduction requirements for fuels across the regulations. By way of example, UK SAF Mandate has a sub-cap for HEFA and there are variances as regards eligibility of crop derived biofuels. In terms of operation, unlike the EU ETS, UK ETS and SAF Mandates, CORSIA does not impose a carbon emission cap, but rather an offset scheme, requiring airlines to offset emissions over a defined baseline. Under CORSIA, only CORSIA-approved carbon credits can be used for compliance; this is a significantly smaller pool than the broader carbon market.

This creates a challenging landscape for airline operators and fuel suppliers to navigate as they either need to have different SAF for different flight plans or narrow the SAF supply to such SAF which is compliant to all their relevant flight plans and associated regulations (the latter in practice is more likely).

"Airline operators face multiple reporting regimes, verification standards and are subject to scrutiny from several enforcement authorities."

This lack of a harmonised regulatory landscape risks fragmenting the SAF market and complicating certification processes, raising questions about cross-border recognition of SAF compliance and potential trade disputes. Furthermore, it means airline operators face multiple reporting regimes, verification standards and are subject to scrutiny from several enforcement authorities.

With a view to providing clarity and certainty to industry stakeholders, the European Commission has adopted a new Delegated Regulation to standardise how aviation emissions are monitored, reported and verified under the CORSIA scheme within the EEA.

This article focusses on EU and UK applicable SAF and carbon reduction regulations in the aviation sector and it should be noted that the landscape described above will be further complicated by SAF and carbon reduction regulations applying to flights emanating from countries outside the EU and the UK and the associated regulations. We note that several countries in Asia, as well as Australia, New Zealand, Brazil, Chile and Türkiye have already or are introducing their own SAF Mandates. We will be exploring SAF mandates in other markets in future articles.

In the next article of this series, we will examine the impact of the SAF Mandates and carbon emission reduction regulations on the SAF market and whether now is the time to start investing in SAF production facilities given the economic viability of manufacturing and supplying SAF.

Footnotes

[1] Source: https://european-union.europa.eu/easy-read_en

Key contacts

Partner London

Partner London