One constant in the ever-evolving world of international trade is that access to capital is critical to the operations of suppliers, traders and end-users of commodities. However, the allocation of capital serving the sector has undergone a transformation in recent years, becoming increasingly scarce, channelised and concentrated amongst the bluebloods of the industry, leaving more recent entrants and smaller participants stressed for funding. The commodity-backed structured trade finance industry, or “STF”, has stepped in to address this gap in the market.

STF is a self-liquidating, collateralised, and de-risked approach to trade finance, tailored to address the foregoing gap. It is a specialised form of financing that facilitates the movement of physical commodities across global markets and monetises global supply chains to unlock funding. It is widely used in the oil & gas, metals and agricultural sectors where transactions involve complex supply chains, multiple jurisdictions and fluctuating prices. The collective of the structures deployed for such financings are referred to as STF and these structures can range from simple repurchase transactions, prepayments to complex project financing coupled with offtakes.

This article introduces STF structures and discusses the complexities and risks surrounding this, arguably esoteric, branch of trade finance.

Understanding STF

STF structures enable commodity trading principals and financiers to provide alternative funding solutions to borrowers by leveraging the value of underlying assets and contractual flows. They commonly involve the following:

- physical commodity flows;

- collateralisation of goods or receivables;

- ring-fenced cash flows from offtakers or third-party buyers;

- security, including over assets and underlying goods;

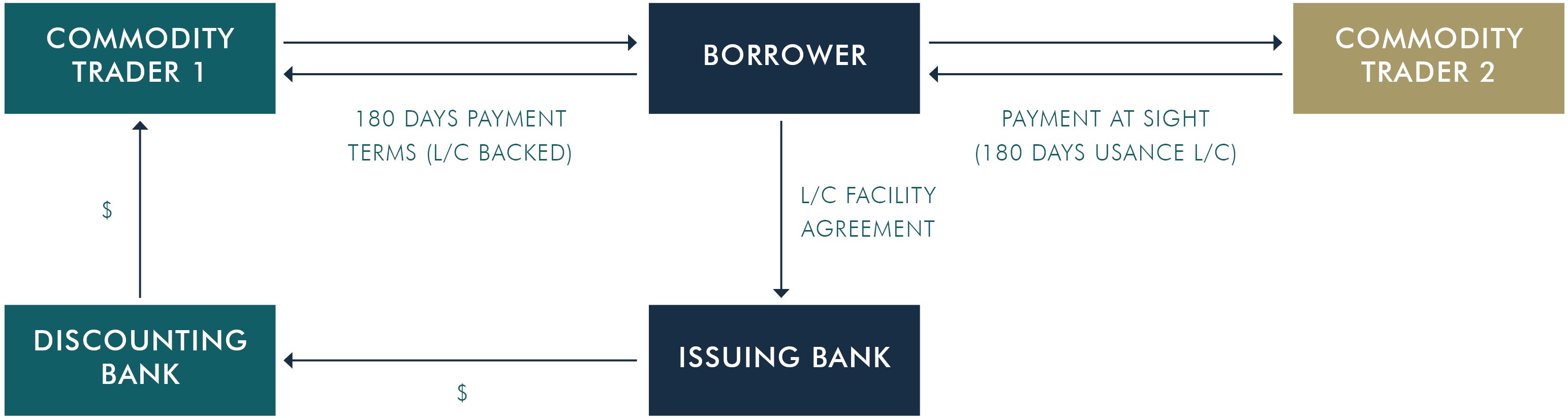

- payment instruments including LCs, SBLCs, bills of exchange, promissory notes, or corporate guarantees; and

- insurance.